The Hormuz shock didn’t break Europe's gas market—time might

Europe's natural gas market has passed the Hormuz stress test—at least so far. A U.S.-Iran peace deal suggests the worst of the shock may be over, even if flows recover only gradually. That should temper supply fears and shift attention to the demand pressures likely to shape the market in coming decades.

The near-total closure of the Strait of Hormuz following the outbreak of the U.S.-Israeli war with Iran halted nearly 20% of global liquefied natural gas trade, sending Asian and European gas prices sharply higher.

Even though the Strait is expected to reopen under the deal, tanker operators warn transit could take weeks to resume, while LNG producer QatarEnergy has reported that Iranian attacks wiped out 17% of its capacity for up to five years.

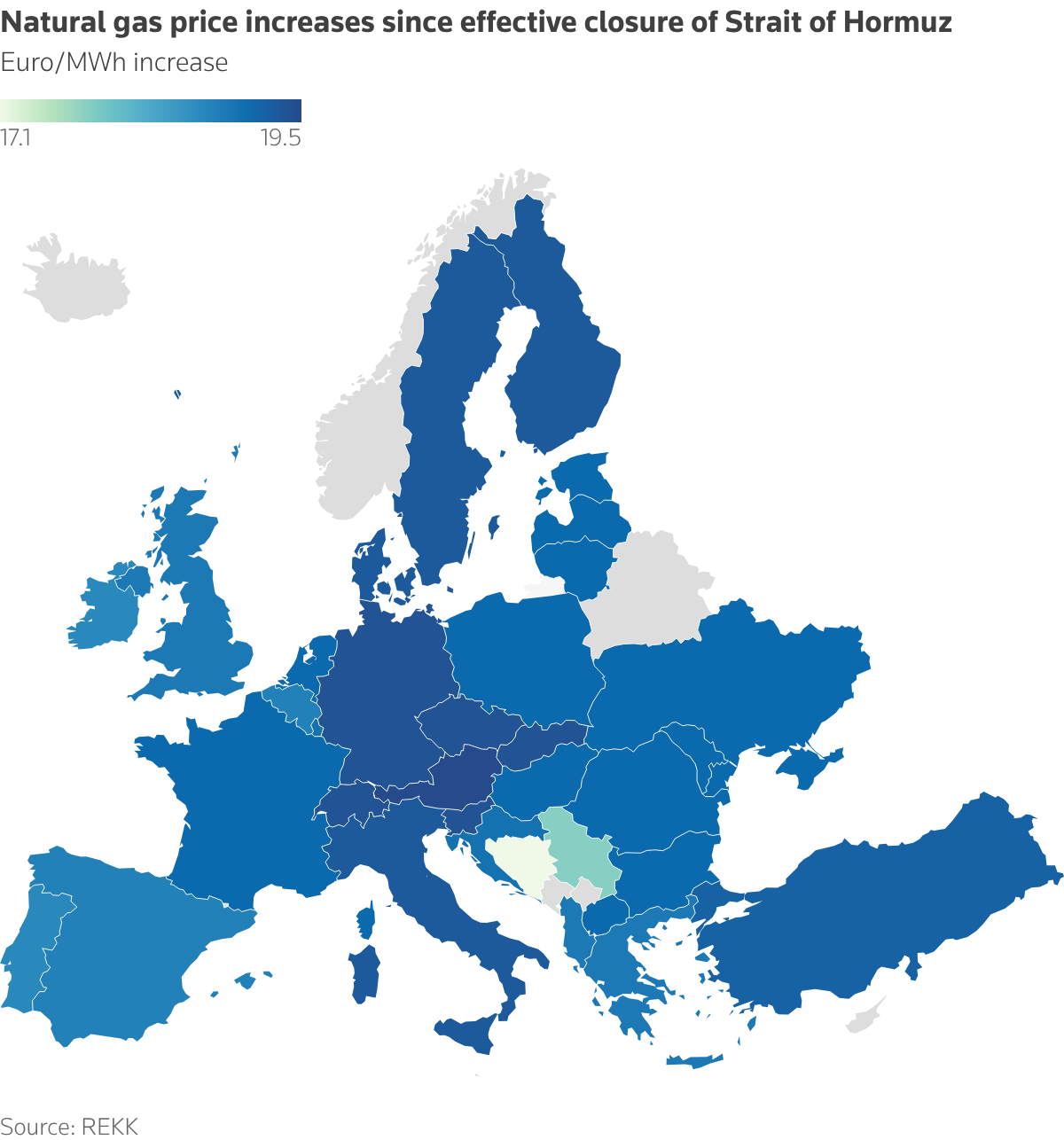

Average European prices have surged by around €10 per megawatt hour (MWh), or roughly 31%, since the start of the conflict on February 28. The total gas bill for the 27 European Union countries has ballooned by 48% this year during the crisis.

Yet the shock has not broken Europe's gas market.

Europe was able to draw on abundant U.S. deliveries and larger volumes from Algeria and Nigeria to help plug the Hormuz-sized hole.

Moreover, the system has not fragmented into competing regional zones. There have been no major infrastructure bottlenecks, and price jumps have remained broadly equal across member states. Pipelines, LNG terminals and interconnectors helped preserve market solidarity under severe stress.

That does not mean the shock was painless, of course. For one, Russian LNG imports rose roughly 17% in January–May, according to preliminary LSEG data, even as Europe seeks to sever energy ties with Moscow over its 2022 invasion of Ukraine.

But overall, Europe’s gas system proved remarkably resilient, especially considering the scale of the supply shock – and appears capable of absorbing more.

A more severe shock combining a Hormuz-style disruption with a full ban on Russian gas was modeled.

In this scenario, European gas prices would rise by only an additional €0.4–€0.8 per MWh in Western Europe and €1.1–€1.4 in Central and Eastern Europe - about 7% of the increase seen since Hormuz closed.

The relatively modest increase reflects Europe's ability to replace most Russian volumes with additional LNG imports through new regasification terminals in the Baltic, Adriatic and Aegean Seas. Expanded interconnector infrastructure in the CEE region and some reduction in demand also limited supply bottlenecks.

This suggests that fears about future supply constraints on the continent — most notably among those who oppose the total phaseout of Russian gas — may be overblown. The bigger risk lies on the demand side, where the outlook is far bleaker.

Demand destruction. Europe’s future gas demand appears set to decline sharply in the coming decades.

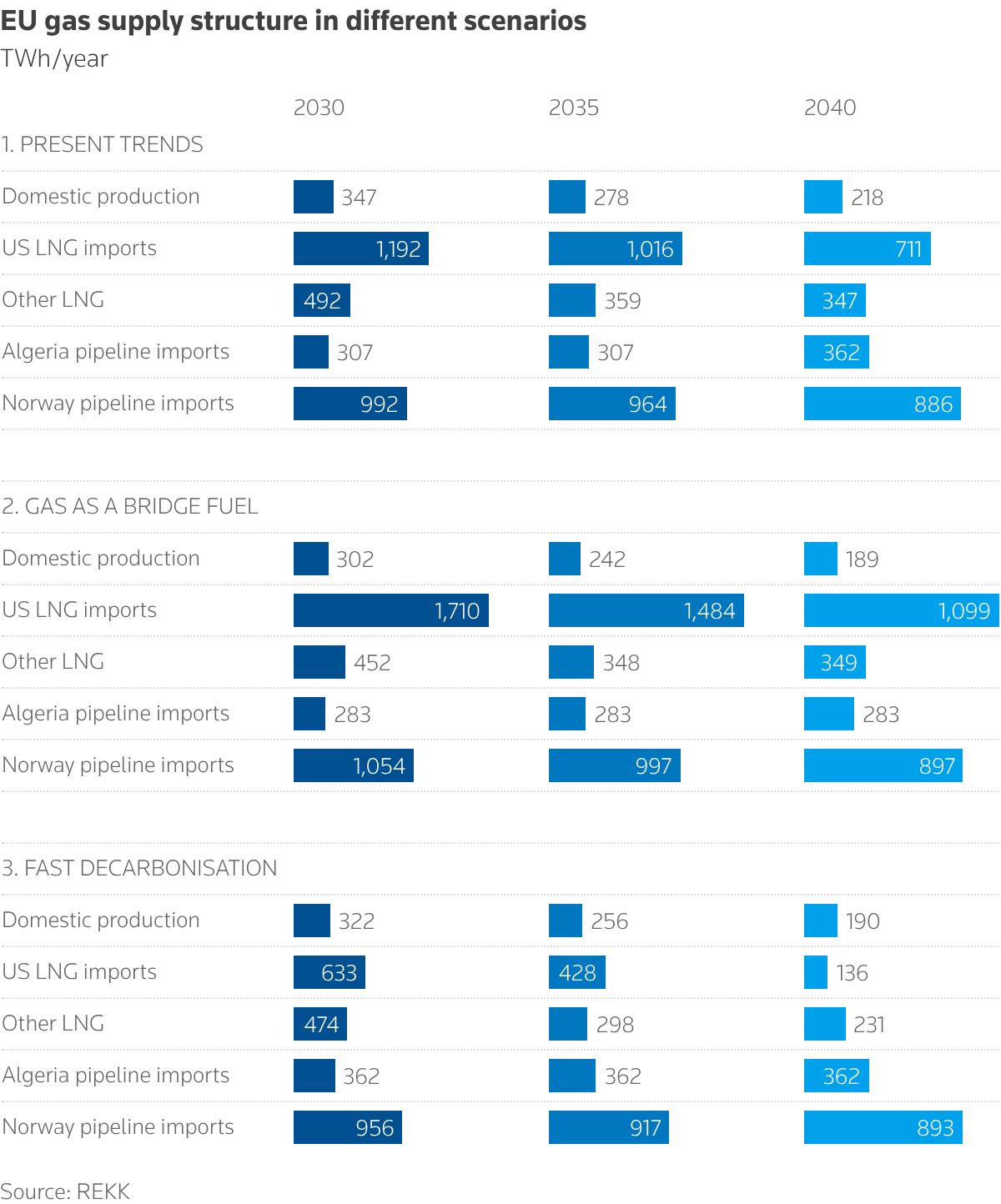

That is the conclusion of a joint modelling assessment recently completed by our think tanks, the Regional Centre for Energy Policy Research (REKK) and the Center for the Study of Democracy (CSD). We assessed the EU's energy demand outlook through 2040 under three scenarios: current trends, rapid decarbonization, and greater reliance on gas as a bridge fuel.

The slope of the downward curve depends, unsurprisingly, on global gas prices.

In the bridge-fuel scenario, we anticipate European wholesale prices averaging around €25/MWh - about 50% below the Iran shock levels - supported by abundant global LNG supply. At those prices, gas-fired plants would remain competitive, coal would be phased out faster, and industrial users could keep using gas while waiting for low-carbon alternatives.

Even so, we estimate that total EU gas demand would still fall by around 30% from 2030 to 2040, to around 2,700 terawatt-hours (TWh) per year, driven by efficiency gains in the residential sector and rapid electrification in industrial segments where electricity would likely replace gas for heat generation.

In the scenario assuming current trends continue, average European gas prices would remain closer to €35. Gas would likely still play an important role in balancing power markets, with gas-fired plants ramping up generation, especially when renewable output is low.

Yet its economics would probably become significantly less attractive in buildings and industry, where higher prices would increase the incentive to electrify. As a result, annual gas consumption would fall further, to around 2,300 TWh.

The business case weakens further in the accelerated decarbonization scenario, where tighter global LNG markets and recurring geopolitical disruptions push gas prices towards €65. At these levels, gas consumption would be expected to decline rapidly across almost all sectors, reaching around 1,700 TWh - roughly half the level in the most bullish demand scenario.

In this environment, power systems would likely rely increasingly on renewables, batteries and new nuclear plants, while electrified heating would become the norm in buildings. European industry would also face growing pressure to cut consumption, electrify where possible and improve efficiency.

Concentrated supply. On the supply side, Europe's options may become more limited over time. Qatar - the world's second-biggest exporter of LNG - is likely to redirect a larger share of its LNG exports toward Asian buyers, given rapidly rising energy needs in the region.

As a result, U.S. LNG is projected to dominate the European market in all our scenarios. U.S. volumes already make up around 60% of total European LNG imports, a share that we expect to rise to 80% by 2030 in a scenario where Europe fully phases out Russian gas as planned.

This dependency - alongside the risk of a more fragmented trading environment - suggests that our high-price scenario is becoming increasingly realistic.

Of course, these are only scenarios, based on assumptions that may not be borne out.

However, these findings challenge a widespread assumption in Europe's energy debate: that gas can comfortably serve as a cheap transitional fuel for decades. If LNG prices stay structurally high because of global competition and recurring geopolitical disruptions, Europe's transition away from gas may accelerate regardless of policy targets.

Gradual erosion - rather than sudden collapse - may ultimately define Europe's gas story.

Related News

Related News

- Cheniere signs deal with Bechtel to expand U.S. LNG export capacity

- TC Energy approves $1.5-B Columbia Gas expansion after profit tops estimates

- Wärtsilä continues to expand its data center footprint with new 790 MW order in Texas

- Baker Hughes’ fuel flexible NovaLT™ 16 gas turbine certified by RINA for marine propulsion

- Japan got bulk of Russian LNG from Sakhalin-2 in 2025

Comments