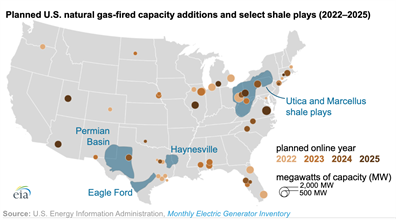

Most planned U.S. natural gas-fired plants are near Appalachia and in Florida and Texas

Between 2022 and 2025, 27.3 gigawatts (GW) of new natural gas-fired capacity is scheduled to come online in the United States, according to the EIA's latest monthly electric generator inventory. This added capacity would increase current capacity (489.1 GW as of August 2021) by 6%. Many of the planned natural gas-fired capacity additions are located close to major shale plays in the Appalachia region and Texas and in Florida.

The Appalachia region’s Marcellus and Utica shale plays stretch across Ohio, Pennsylvania, and West Virginia. These shale plays have led the growth in U.S. natural gas production over the past several years, accounting for 34% of U.S. dry natural gas production in the first half of 2021.

Illinois, Michigan, Ohio, and Pennsylvania—states with pipeline access to natural gas from the Marcellus and Utica shale plays—account for a combined 43% of the natural gas-fired capacity planned to come online between 2022 and 2025. Among these four states, Illinois has the most natural gas-fired capacity additions (3.8 GW), followed by Michigan (3.2 GW), Ohio (2.9 GW), and Pennsylvania (1.9 GW). Natural gas transport infrastructure continues to be added to this region to increase pipeline takeaway capacity and to bring natural gas to demand markets in the Midwest, Northeast, Southeast, and Canada.

After Illinois, Florida has the second-most natural gas-fired capacity additions planned to come online between 2022 and 2025 (3.2 GW). Although Florida does not produce significant amounts of natural gas, its regional pipeline networks have been continually expanding to serve natural gas-fired generation units as older coal-and-oil-fired units retire. Five new natural gas-fired plants plan to start commercial operations in Florida between 2022 and 2025: three plants are currently under construction, and two plants are not yet under construction but are scheduled to be completed by 2024.

More natural gas is produced in Texas than any other state. Most of its natural gas production comes from the Haynesville and Eagle Ford formations and multiple shale formations in the Permian Basin. As of August, 70.7 GW of natural gas-fired capacity is currently operating in Texas, and another 2.8 GW of capacity additions is planned to come online between 2022 and 2025. Growth in natural gas production in Texas has encouraged natural gas-fired capacity additions and regional pipeline expansions to accommodate growing natural gas exports to Mexico, as well as record-high LNG exports from terminals in South Texas and in Louisiana.

Principal contributor: Max Ober, Scott Jell

- Mitsubishi Heavy Industries Compressor acquires Swiss rotating equipment maintenance company AST Turbo AG

- RWE strengthens partnerships with ADNOC and Masdar to enhance energy security in Germany and Europe

- TotalEnergies and Mozambique announce the full restart of the $20-B Mozambique LNG project

- Cook Inlet LNG advances FSRU project in Alaska (U.S.)

- Qatar’s Ras Laffan LNG hub hit by missile attack, ‘extensive damage’ reported

Comments