Industry Perspective

M. F. Farina, GE Oil and Gas, Denver, Colorado

Natural gas is poised to capture a larger share of the world’s energy demand. Gas is shifting from a regional, and often marginal, fuel to becoming a focal point of global energy supply and demand. This trend offers the potential for the industry to grow by nearly 35% by 2025—driving gas to 26% of primary energy supply.

However, the industry is at a critical juncture. The costs of mega-gas projects have been spiraling upward, and environmental scrutiny continues to intensify. In Europe, debates swirl on competition and security of supply; meanwhile, coal consumption is climbing as gas-fired power plants sit idle. Market prices remain too low in some regions to invest in supply and infrastructure, while tight markets and high prices keep gas uncompetitive in others. More broadly, geopolitical tensions undermine the collaboration required to link gas supplies between regions. The inability of stakeholders to coordinate on trading terms has left huge deposits of resource as “stranded.”

Elsewhere, immature institutional structures have slowed growth or resulted in costly externalities like gas flaring. It is easy to see why caution has arisen on industry prospects. However, beneath the negative headlines, there is a deeper industry transformation underway—one that was deemed impossible only a few years ago.

Several key forces are driving this transformation in structure and scale. First, advances in unconventional gas, including shale-based resources, are boosting supplies and shifting perceptions about gas availability. When combined with new frontiers of conventional gas development like East Africa, Southeast Asia, and the Mediterranean, gas supply diversity is increasing.

Second, constraints on incumbent fuels like oil and coal are increasing, even as energy demand growth remains strong in vast parts of the developing world. The flexibility, versatility and relative cleanliness of gas as a fuel will be critical to meeting the growing energy needs of emerging markets.

Finally, massive investments in energy networks—gas systems in particular—are underway. Gas pipeline and LNG spending over the last five years represented about 25% of gas industry capital expenditures. This number is expected to increase to 30% over the next five years as transport system spending outpaces the growth in gas upstream exploration and development spending. These factors, combined with the competitiveness of gas, are driving expectations of fast growth.

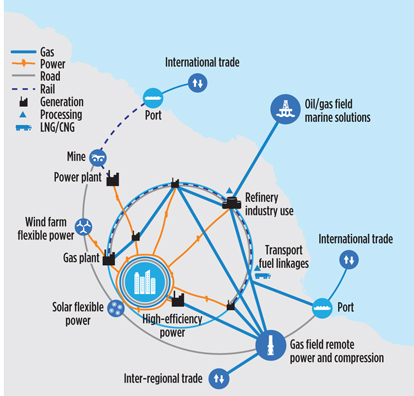

Gas network mega-trends. In looking at the multiple forces driving gas industry development, network growth is critical. The Age of Gas will not happen without greater systematic attention to the need for further building out gas networks and expanding links between various energy systems (Fig. 1).

|

|

Fig. 1. Natural gas systems integrate with other energy networks. |

An important aspect of gas networks is that, as systems integrate or become denser, they also become more valuable. New networks create opportunities to bring buyers and sellers together. The end result is network growth that contributes to lower costs and greater flexibility in the system, which, in turn, fosters further growth. The additive nature of gas networks is one of their essential features. Regardless of how they were built and paid for, the key is that interconnections are allowed, and access can be secured or provided in an economic way.

Gas networks will grow differently in different regions. Those regions early in the industry development phase, like Mozambique and Myanmar, are investing in building point-to-point and hub-and-spoke networks. Growth regions like China, Indonesia and Brazil are extending gas networks and integrating LNG or CNG systems with traditional pipelines. In the EU and the US, where gas networks are mature, there is increasing potential for synergies across multiple large networks. From these observations, three important gas network mega-trends are emerging:

- Twin development pathways. Gas networks are expected to grow along parallel pathways. Mega-pipeline and LNG projects will continue to “anchor” gas network growth. This is the traditional growth path for the linking of large gas supply resources to demand centers. However, these networks will be augmented with a next generation of smaller modular systems. These networks can serve small power-generation systems, light industry, fleet fueling stations, etc. These “satellite” systems offer fast alternatives to traditional developments. They can be built around large networks or completely isolated. Examples include the small-scale LNG and CNG systems being built near new pipelines or regasification terminals in China, or those designed to replace diesel use in the remote mining operations of Australia, Indonesia and Canada.

- Deeper gas system integration. Over the next decade, tighter integration between pipelines and LNG is expected. LNG and CNG system expansion may outpace pipeline development, bringing flexibility to old pipelines and new avenues for competition. For example, the number of countries importing LNG (25 today) could nearly double by 2020. Approximately two-thirds of these countries already have domestic supply or pipeline gas; as a result, LNG will diversify and deepen the gas supply options for these countries.

- Future network integration. Integrated gas networks will create more opportunities for links with other energy networks. Networks tend to be developed and considered in isolation, but are operated in conjunction within the context of larger systems. There is growing recognition that the fuller integration of networks creates additional reliability and energy security. The natural gas system is uniquely positioned to support other energy networks. Furthermore, as gas systems become more intelligent with new digital and software technologies, these benefits will likely grow. The idea of multi-network optimization focuses on using technology to proactively facilitate network switching.

Market evolution. One implication of increasing supply diversity and “denser” gas networks will likely be the formation of a more “hybrid” gas market. Many elements of the traditional, vertically integrated monopoly gas business will be slow to change, but increasingly competitive and flexible trading networks are coming. The industry will be pushed to become more dynamic, with short-term contract lengths and more spot trading. In addition, expanding networks will likely drive price convergence.

Regional prices will remain different, but more because of the underlying cost of supply and transportation and less because of strict contractual linkage to oil. Today, long-term contracts implicitly contain elements of balancing, flexibility and storage, even as they underwrite large capital investments in upstream and midstream infrastructure. The evolution away from traditional models will require more transparency on the cost of various gas services. Transparency will be especially important as gas and power systems converge.

Policy considerations. Government policy will be another key element shaping the development of gas systems. For emerging gas economies, the expansion of gas networks starts with national energy planning and regional government engagement. Early thinking on developing energy systems in a scalable and modular way is important. Consideration should be given to establishing the role of the regulator, including how access to networks will be managed and what revenue model will support investment. These considerations can have significant implications for how systems are managed for open access, cost of services and transparency.

Reducing the environmental footprint of gas operations will be another focal point for the industry. Specifically, this means redefining what is possible in gas operations, including diesel substitution, improved water management for shale, reduction of fugitive emissions, and new concepts for efficiency and electrification.

Tailored solutions will also be important. For countries trying to develop new gas infrastructure, a solid legal foundation and reputation that support direct foreign investment and contracting are essential. The ability to efficiently develop effective public-private partnerships is imperative. International companies are willing to take financial and operational risks to develop resources, build infrastructures and link markets, if governments can create a stable business environment.

The Age of Gas. A world in which natural gas can take on a much larger role in the global energy mix is a real possibility. Put simply, the trend is toward growing gas availability, better deliverability and more marketability. Global gas demand today is about 3,500 billion cubic meters per year (Bcmy), or about 70% of the size of the global oil market. Global gas consumption can grow by nearly 1,300 Bcmy by 2025. Over half of the incremental growth in this period will take place in China, the Middle East, and South and Southeast Asia. Over that period, LNG demand is expected to increase by over 280 Bcmy, nearly doubling the size of the global LNG market.

Given that so much growth will occur in areas with immature energy networks and often young institutions, governments that do a good job of getting early infrastructure models right will be better positioned for future growth. Policymakers should focus on correctly aligning networks for their country’s situation.

Furthermore, developers of midstream systems and processing operations should recognize how gas systems can integrate in the broader regional energy market. Optimized networks for power, gas, transportation and renewable energy may allow access to new markets and higher utilization rates. There may be benefits that traditional isolated business models fail to recognize, such as spreading costs over a more diverse customer base, or capturing the value of higher levels of resiliency and environmental performance.

The gas networks required to realize the Age of Gas do not yet exist, although many elements are in place in some parts of the world. Only with a combination of state-of-the-art technology, sustainable practices and continuing collaboration will the potential of natural gas be realized. GP

|

MICHAEL F. FARINA is a senior manager of strategy and analytics with GE Oil and Gas. He has been involved in a number of key strategic efforts with GE focused primarily on natural gas, including unconventional gas initiatives and flare gas reduction strategies. Most recently, Mr. Farina was lead analyst and co-author of GE’s “Age of Gas and the Power of Networks” white paper. He has been with GE for six years, and in the oil and gas industry for almost 20 years. Previously, Mr. Farina was a director of natural gas consulting at Cambridge Energy Research Associates (CERA). He holds a BA degree in economics from Colorado State University and an MA degree in economics from the University of Colorado.

Comments